I continue to see a risk off environment in equities that has spilled over to emerging markets. The consensus from American conglomerates on China demand and now Chinese data itself is pointing to significant economic contraction in China. The markets in

Turkey (TUR),

Vietnam (VNM) are holding strong. Vietnam continues to be my favorite opportunity in emerging markets over the long-term.

Last week Bitcoin saw increased selling and volatility. This just adds to the risk off sentiment as Bitcoin, one of the best performing assets this year is joining in on the selling. Below is the breakdown of the trend support currently in the works on Bitcoin. I alerted on the recent

top for Bitcoin here on the blog in early 2022.

In light of this overall market weakness I see opportunity in pharmaceuticals with ETF's like

VanEck Pharmaceutical ETF (PPH) and

I-Shares Pharma ETF (IHE). The ETF's have recently broken out to new 52 week highs and shown relative strength in the market. I'm particularly bullish on the sector because breakthroughs in AI machine learning should improve drug development costs and increase speed of discovery and research.

I've done extensive research on the newest AI via large LLM's(large language models) and the promise of smaller ones. Drugs and biotech are some of the industries they will transform initially. They are the perfect fit for industries where scanning large language databases is key and processing large amounts of data is needed.

The pharma ETF

PPH is coming up on a key support level.

Merger Arb Opportunities

There are opportunites in merger arbitrage with Spirit Airlines (SAVE) and I-Robot (IRBT). Spirit is trying to get an all cash deal done with Jetblue for $33.50 a share. Amazon has been in the works and shareholder approved to buy I-Robot for all cash or $51 a share too.

Oil and Gas Energy

Apart from pharma I have seen relative strength in energy stocks. I have particularly been looking at oil and gas stocks as natural gas has pretty much been written off. I'm not particularly bullish on natural gas but the contrarian trade now is nat gas as harsh winter weather is likely not priced in. The best gas ETF is US 12 month Fund (UNL) at it holds long dated contracts and thus has less decay than ETF (UNG). Nobody is bullish on natural gas prices as the technicals have shown a bottom formation forming.

Some of the energy stocks I added to my watchlists were VAALCO (EGY),Helix Energy (HLX), Nextier Oilfield (NEX), KLX Energy (KLXE).

Solar Weakness Continues

Another industry that caught my attention was Solar. It caught my attention as a short opportunity as the weakness in solar continues as evidenced by the Invesco ETF (TAN). I noticed short selling technical setups in stocks like JKS and MAXN too.

I'm bullish on the prospects of breakthrough technology like quantum computing with the help of AI. The quantum computer ETF is Defiance Quantum ETF (QTUM). I also particulary like the quantum computing stock Rigetti Computing (RGTI) as they have one on the cloud.

I continue to believe the investment of our lifetimes going forward will be in artificial intelligence. The best plays on this are the actively managed Roundhill ETF (CHAT) and long established Global X AI ETF (BOTZ) and Robo Global ETF (ROBO).

One good speculative investment opportunity I saw was in the Nigeria country specific Nigeria ETF (NGE). Nigeria NGE has a trailing twelve month 16% dividend yield. 0.83% expense ratio. Politics might be a partial driver of the 28% YTD performance of Nigerian stocks.

"The Tinubu admin also formed a committee on fiscal policy and tax reforms headed by Taiwo Oyedele, signalling the possibility of critical tax reforms"... " Banking and oil gas stocks have been very strong drivers of market performance. Oil and Gas stocks have been on the rise since they took out fuel subsidy from the sector. Added with banking, they are the top two sectors.”

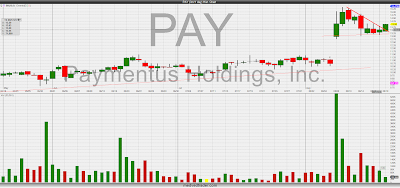

On specific stocks on the long side I see a buy setup in Payments Holdings (PAY) as it saw large buying volume after earnings and is consolidating in a flag now. It needs to hit 14.05 for a long trade. The company has strong revenue and earnings growth. They recently revised quarterly earnings forecasts to the upside. Next years earnings guidance has been raised to $.24 EPS vs previous $.14.

Full disclosure:

I have been actively trading the PPH ETF, RGTI. I have puts on JKS, long BOTZ, CHAT. May long NGE in future.